When we talk about cyber security in accounting, we're talking about protecting the lifeblood of your firm: sensitive financial data, client information, and the very systems you use every day. This isn't just an IT problem to pass off to the tech team—it's a core business responsibility. Why? Because accounting professionals are sitting on a goldmine for cybercriminals, holding everything from tax records and payroll information to confidential corporate financials.

A strong defense isn't optional. It’s absolutely essential to prevent devastating breaches and maintain the trust your clients place in you.

Think of your accounting firm as a digital bank vault. It might not hold stacks of cash, but it safeguards something far more valuable to modern thieves—a centralized trove of client financial data, tax returns, and personal information. This reality makes accounting firms a high-priority target, demanding a laser-focused approach to digital defense.

The vulnerabilities are woven directly into your daily workflows. Managing payroll, processing invoices, handling sensitive corporate financials—every single task involves data that attackers are desperate to get their hands on. The risk isn't just about losing files; it's about the real-world fallout of a breach.

The financial sector, accounting included, consistently gets hit with some of the highest costs from security incidents. Data breaches in this industry average a shocking $5.56 million per incident, which is significantly higher than the global average of $4.44 million. With global cybercrime costs projected to hit $10.5 trillion annually, it’s crystal clear why the stakes are so high for anyone managing financial data.

That massive number only scratches the surface. The true damage runs much deeper and includes devastating, long-term consequences:

Treating cyber security in accounting as just another IT chore is a critical, and common, mistake. It’s a fundamental pillar of modern practice management, every bit as important as professional ethics and financial accuracy. This guide will walk you through the essential components of building a strong defense, from understanding the most common threats to meeting complex compliance demands. We will also explore the critical relationship between cybersecurity and accounting practices in more detail.

Ultimately, robust security is not just about protecting data; it's about safeguarding your firm's future, reputation, and the financial well-being of the clients who depend on you. It is a non-negotiable aspect of professional responsibility.

If you want to defend your firm, you first have to understand the opponent. Cyberattacks aren’t just random bits of digital chaos; they’re carefully planned operations designed to hit specific weak spots. For accounting firms, those weak spots are almost always the high-value data you handle and the trusted relationships you work so hard to maintain with clients.

Instead of getting lost in technical jargon, let’s break down the most common cyber threats from the perspective of your day-to-day workflow. Once you see how and why these attacks are so effective, building a solid defense becomes much clearer.

The table below gives a quick overview of the threats we'll cover, how they work in an accounting context, and the damage they can cause.

| Threat Type | How It Works | Potential Impact |

|---|---|---|

| Phishing | Attackers send deceptive emails posing as clients, partners, or software vendors to trick employees into revealing passwords or transferring funds. | Direct financial theft, stolen login credentials for accounting software, and network-wide malware infections. |

| Ransomware | Malicious software encrypts all your firm's data—tax returns, financial statements, client files—making it inaccessible until a ransom is paid. | Complete operational shutdown, massive financial loss, destroyed client trust, and potential regulatory fines. |

| Credential Theft | Criminals use stolen usernames and passwords (often from phishing attacks) to log into your systems and operate undetected as a legitimate user. | Silent data exfiltration, invoice and payroll fraud, and setting the stage for larger, more destructive attacks. |

Each of these threats exploits a different vulnerability, but they all lead to the same place: financial loss, reputational damage, and a massive operational headache.

Phishing is easily the most common and wickedly effective attack out there. It’s a form of social engineering where a scammer sends a fraudulent message designed to trick someone into revealing sensitive information or installing malware.

Think of it as a counterfeit check in a digital world. During the chaos of tax season, an email lands in an employee's inbox that looks like it's from a senior partner. It has the firm’s logo, an urgent tone, and a request for an immediate wire transfer for a "confidential client matter." The employee, trying to be helpful and efficient, clicks the link or processes the payment.

That one simple action can unleash a storm of problems:

Phishing works because it preys on human trust and the fast pace of accounting work. Attackers know your busy seasons, your key clients, and the language you use, which makes their fake messages incredibly believable.

If phishing is a quiet heist, ransomware is a hostile takeover. This nasty type of malware encrypts your files, locking them up and making them completely useless until you pay a ransom. For an accounting firm, this is a nightmare scenario, especially if it hits right before a major filing deadline.

Imagine your entire server—client tax documents, financial statements, payroll records—is suddenly inaccessible. A message pops up demanding a six-figure payment in cryptocurrency for the decryption key. Every minute you're down costs you money, damages client trust, and puts you at risk of missing legal deadlines.

This threat is growing at an alarming rate. Globally, security breaches jumped 75% year-over-year, with companies facing an average of 1,876 attacks each quarter. Ransomware has become a favorite tool for criminals targeting the financial sector because the pressure and stakes are so incredibly high. To get a handle on this, check out our guide on how to prevent ransomware attacks and protect your firm.

Credential theft is the digital version of a master key falling into the wrong hands. Once an attacker steals a valid username and password—usually through a phishing attack—they have legitimate access to your systems. They can log into your cloud accounting software, email accounts, and client portals just like any other employee.

Once inside, they can operate for weeks or even months without being detected, causing all sorts of damage:

Because the attacker is using valid login details, traditional security tools like firewalls might not see anything wrong. This is what makes credential theft one of the most dangerous threats to cyber security in accounting—the breach happens from the inside out.

Knowing the threats is one thing; stopping them is another. The only way to neutralize them is by building a layered defense, a digital fortress around your firm’s most sensitive data. This involves a smart mix of technical tools and airtight administrative rules.

Each layer is designed to slow down, block, and expose potential attackers, making your firm a much harder—and far less appealing—target. Think of it less like a single, massive wall and more like a series of checkpoints, reinforced doors, and security patrols. An intruder might slip past the first guard, but the others are ready and waiting.

We’ll start with the foundational controls that give you the biggest bang for your buck and build from there, creating a security posture that’s genuinely tough to crack.

The front door is almost always the weakest link. Most attackers get in by using weak or stolen login credentials. That’s why the single most critical layer of your defense is strengthening how people access your systems.

Multi-Factor Authentication (MFA) is the undisputed champion here. Imagine your password is the key to your office door. MFA demands a second, separate key before letting anyone in—usually a one-time code sent to a trusted device like your smartphone.

So even if a cybercriminal manages to steal a password, they’re stopped cold. They don't have that second key. For a comprehensive approach, combining technical controls like MFA with essential cyber security risk management strategies is a crucial step forward.

Multi-Factor Authentication is your single most effective defense against unauthorized access. Reports consistently show that implementing MFA can block over 99.9% of automated credential-based attacks, making it a non-negotiable security control for any accounting firm.

Once your access points are locked down, the next job is to protect the data itself. Even if an attacker somehow breaches your network and gets their hands on your files, that data should be completely unreadable and useless to them. This is where encryption comes in.

Think of encryption as translating your client’s financial records into an unbreakable code. Only people with the correct decryption key can turn it back into plain English. This needs to happen in two places:

This proactive step ensures that even in a worst-case scenario, the sensitive client data you’re paid to protect remains confidential.

Not every employee needs access to every single client file. The Principle of Least Privilege is a cornerstone of cyber security in accounting. It’s a simple idea: users should only be given access to the specific data and systems they absolutely need to do their jobs, and nothing more.

It’s like a keycard system in an office. An employee's card might open the main entrance and their own office, but it won’t unlock the server room or the CEO’s suite. Digitally, this means a junior accountant working on small business accounts should have zero access to your firm’s largest corporate client files. You can learn more about how to implement a Zero Trust security model, which is built on this very principle.

These controls drastically limit the blast radius if an attacker ever compromises a single employee’s account.

Technology is only half the battle. Strong administrative controls are vital for catching internal fraud and honest mistakes. A core practice here is the segregation of duties. This policy ensures that no single person has the power to both initiate and approve a financial transaction.

For example, the person who can add a new vendor to the payment system should not be the same person who can approve and send payments to that vendor. It’s a simple, powerful check and balance.

Finally, your ultimate safety net against a disaster like a ransomware attack is a reliable backup system. Think of your backups as a digital time machine. Regular, tested backups of all critical data allow you to restore everything to a point in time before the attack ever happened. This turns a potentially business-ending catastrophe into a manageable incident, letting you sidestep ransom demands and get right back to work.

Real cybersecurity for accountants is about more than just installing the right software. At its core, it’s about upholding your legal and professional duty to protect the sensitive client information you’ve been trusted with. This responsibility isn’t just a good business practice; it’s governed by a complex web of data privacy regulations that have real teeth.

Failing to comply isn't a simple technical slip-up. It can lead to crippling financial penalties and do permanent damage to your firm’s reputation. These rules aren't suggestions—they're legal mandates that dictate exactly how you must handle personal and financial data.

It’s tempting to treat compliance like a one-time checklist you can tick off and file away. But regulations like Europe's General Data Protection Regulation (GDPR) or the various state-level privacy laws popping up in the U.S. demand something more: an ongoing commitment. They force you to think of data protection as a continuous business process, not a project with a finish line.

This means knowing precisely what client data you have, where it lives, who can touch it, and how it’s secured at all times. It’s about weaving privacy into the very fabric of your workflow, from the moment you onboard a new client to the day you archive their old records.

Compliance isn't a static, perfect state of security. It's about showing you’ve done your due diligence. It’s a living, breathing framework for managing risk, responding to incidents, and constantly adapting your defenses as new threats emerge.

To see how this plays out, let's walk through a common nightmare scenario. Imagine an employee’s car is broken into, and their laptop—containing unencrypted client tax returns—is stolen. This isn't just a lost piece of equipment; it's a full-blown data breach with a clear and painful set of consequences.

Under most regulations, your firm would be legally required to take immediate action:

Juggling all these technical and administrative burdens can feel overwhelming, especially for small to mid-sized firms. This is where a strategic partnership with a secure cloud hosting provider can be a game-changer. A specialized host takes a huge chunk of the technical compliance weight off your shoulders.

When you move your accounting software to a secure cloud, you’re plugging into an infrastructure that was built from the ground up with compliance in mind. These providers deliver auditable systems, managed security controls, and powerful data protection measures that help you meet your obligations. They handle the complex server-side security, so you can focus on your firm’s internal policies and client relationships. For instance, knowing a provider’s certifications is key; you can learn more about what SOC compliance is and how it validates a provider's controls. This kind of partnership makes achieving and maintaining compliance a far more manageable task.

Even with the best defenses in the world, no system is completely bulletproof. That’s why a solid incident response plan is your ultimate safety net. It’s what separates a calm, methodical recovery from a panicked, chaotic scramble that makes a bad situation infinitely worse.

Think of it like a fire drill for a cyberattack. You practice the steps so when a real alarm sounds, everyone knows exactly what to do. A well-crafted plan turns abstract security ideas into a concrete playbook that protects your firm’s reputation and finances during a crisis. It covers everything from the first sign of trouble to a full recovery, ensuring you meet legal notification duties without fumbling.

For a deeper dive, our guide on creating a data breach response plan breaks down the components in even greater detail.

An effective plan is built around a few distinct phases, each with a clear purpose. The goal is to move smoothly from one stage to the next, minimizing damage and downtime along the way. Your plan must clearly define who is responsible for each step.

Here are the critical stages to include:

Phishing and social engineering are still the top threats aimed at accountants, and the attacks are only getting smarter as criminals use AI to mimic trusted contacts. Business email compromise (BEC) was the leading cause of cybercrime losses in Australia during a recent fiscal year, part of 87,400 reported incidents—that’s one every seven minutes.

With breaches in the financial sector costing an average of $5.56 million, the ability to respond in minutes, not days, is absolutely crucial.

Having a plan is one thing; having one that works under pressure is another. Developing a robust strategy for dealing with security breaches is paramount, and understanding effective cyber incident response planning can provide the framework needed to ensure your team is truly prepared for a real-world event. This preparation turns a potential catastrophe into a manageable operational challenge.

Even with a strong defense in place, it’s natural to have questions about how it all works in the real world. Let’s tackle some of the most common concerns we hear from accounting professionals to clarify these key concepts.

It’s a great question. Services like Dropbox are fantastic for simple file sharing, but they aren't built to run your actual accounting software securely. A specialized cloud host takes your entire application suite—think QuickBooks or Sage—and places it in a managed, high-security environment designed from the ground up for both performance and protection.

This dedicated approach offers critical advantages that general cloud storage just can't touch:

While a layered defense is always the goal, the single most effective action you can take is to implement mandatory Multi-Factor Authentication (MFA) across every single system. The overwhelming majority of breaches happen because of stolen or weak passwords.

MFA creates a powerful second barrier that can stop an attacker cold, even if they have an employee's password. It’s a simple step that dramatically reduces your risk of unauthorized access.

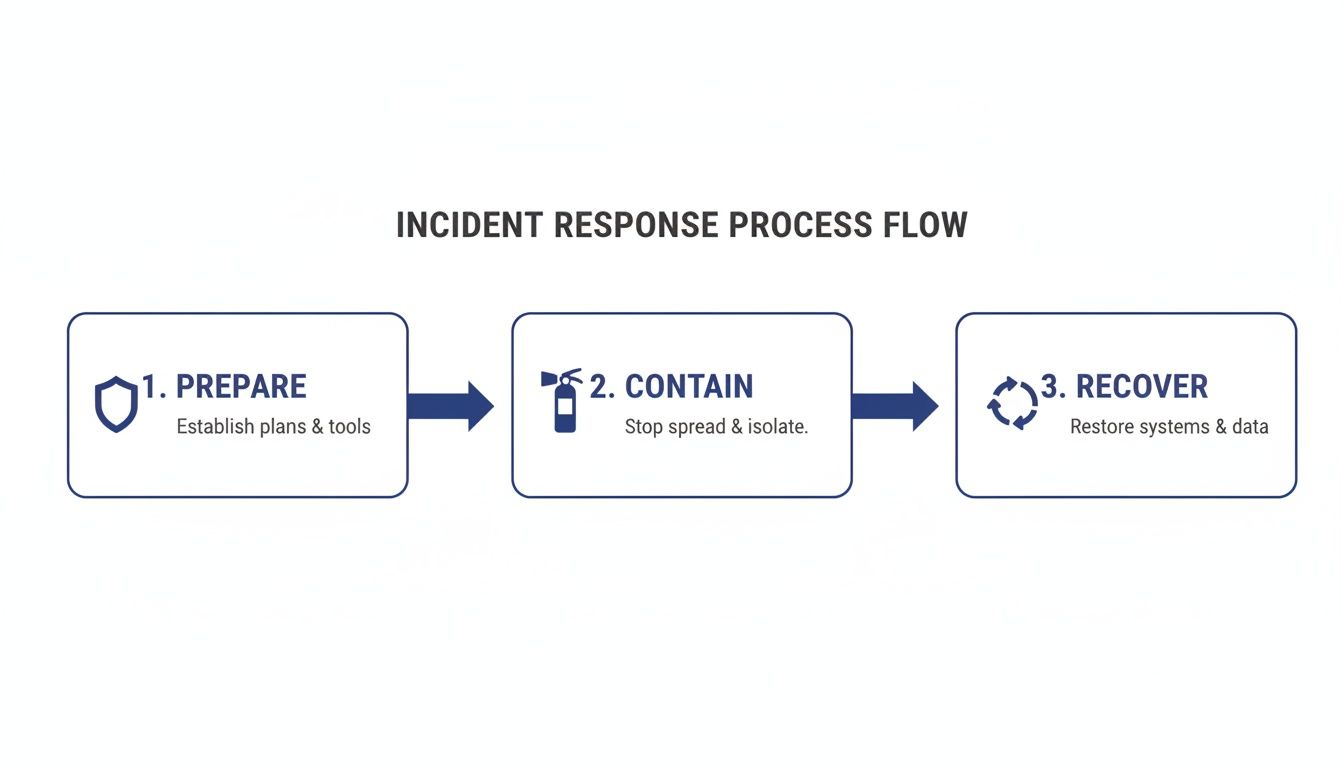

A good security plan also includes knowing what to do when something goes wrong. The process flow below illustrates the key stages of responding to an incident, emphasizing the need for preparation, containment, and recovery.

This visual underscores a critical point: a successful response begins long before an attack ever occurs. Having clear steps in place is what allows you to minimize damage and get back to business efficiently.

Ready to secure your firm's data with enterprise-grade protection? Cloudvara offers a secure, managed cloud hosting solution that centralizes your applications and protects your most valuable asset—your client data. Learn more and start your free trial today.