To a cybercriminal, your accounting firm isn't just another business—it's a treasure chest. Getting cyber security for accountants right is no longer just another IT expense. It's a core survival strategy, the digital equivalent of a bank vault protecting everything from client Social Security numbers to confidential tax filings. This reality demands a proactive defense against threats that can bankrupt a firm and ruin its reputation overnight.

To really grasp the urgency here, you have to learn to see your firm through a hacker's eyes. Stop thinking of your office as a place of business and start seeing it as a digital Fort Knox. Every client file, every tax return, and every financial statement is a bar of gold just waiting for them to snatch and sell.

That isn't hyperbole. Accounting firms are irresistible targets because they conveniently bundle the three most valuable types of data for criminals into one place:

This concentration of sensitive data makes your firm a one-stop shop for cybercriminals. Why bother hacking hundreds of individuals when they can hit one accounting firm and get it all? It’s just more efficient.

Hackers are driven by a simple formula: maximum return for minimum effort. They know that accountants are gatekeepers, holding immense trust and privileged access. Your systems are the doorways to the financial hearts of dozens, if not hundreds, of other businesses and individuals. An attacker doesn't just see your firm; they see your entire client roster as a list of secondary victims.

A successful breach of an accounting firm creates a ripple effect, compromising not just one organization but an entire network of clients. This is why attackers invest significant resources into targeting financial professionals—the potential payoff is exponential.

They also know your calendar. Tax deadlines, payroll runs, and quarterly reports create predictable windows of vulnerability. An attack launched during a chaotic busy season is far more likely to work because your staff is overworked, stressed, and more likely to make a small mistake—like clicking a malicious link in a convincing-looking phishing email.

The fallout from a data breach goes way beyond just stolen money. For an accounting firm, the damage strikes at the very heart of your business model: trust. A single security incident can set off a devastating chain reaction.

Just think about the aftermath:

In the end, strong cybersecurity isn’t an IT problem; it’s a critical business function. It’s the modern-day equivalent of the locked vault and the security guard—absolutely essential for protecting your assets, your clients, and your firm’s future.

Before you can build a solid defense, you have to know what you’re up against. For accountants, cyberattacks aren't just random digital noise; they’re targeted campaigns designed to exploit the specific pressures and workflows of your profession. The bad guys have done their homework. They know your processes, and they know exactly where to hit you.

Let's skip the dense technical jargon and look at the real-world scenarios that play out in accounting firms every single day. These aren’t hypotheticals—they are active, persistent dangers that demand your full attention. Understanding how these attacks work is the first step for anyone serious about cyber security for accountants.

To get a clearer picture, here’s a quick rundown of the most common threats your firm is facing right now.

| Threat Type | How It Works | Primary Impact on an Accounting Firm |

|---|---|---|

| Business Email Compromise (BEC) | Attackers impersonate a partner or trusted client via email to trick staff into making fraudulent wire transfers or revealing sensitive data. | Direct financial loss, breach of client trust, and potential legal liability for unauthorized fund transfers. |

| Ransomware | Malicious software encrypts all your firm's data, making client files, tax software, and records inaccessible until a ransom is paid. | Complete operational paralysis (especially during tax season), catastrophic data loss, severe reputational damage, and costly downtime. |

| Insider Threats | A current or former employee intentionally or accidentally exposes sensitive data, either through negligence (losing a device) or malicious action. | Data leakage of confidential client information, compliance violations (violating FTC Safeguards), and erosion of client confidence. |

Let's dig a little deeper into what makes these attacks so effective and why accountants are such a prime target.

Picture this: It's the chaotic end of the quarter, and an urgent email lands in your inbox from a senior partner. It looks completely legitimate—right down to their signature and professional tone. The message instructs you to process an immediate wire transfer to a new vendor to close a time-sensitive deal. Under pressure, you make the payment.

Only later do you discover the partner never sent that email. You’ve just wired a huge sum of money directly into a criminal's bank account.

This is Business Email Compromise (BEC). It's a dangerously effective scam that leans on impersonation and social engineering, not on fancy hacking. Attackers meticulously research your firm’s hierarchy, pinpoint key decision-makers, and use what they learn to craft incredibly convincing fake requests. They prey on the inherent trust and authority within your firm's structure.

Business Email Compromise (BEC) has become the number one source of cybercrime-related losses in the accounting world. In fact, research from Australia's FY2023–24 identified BEC as the leading cause of such losses, with accounting firms facing attacks at a staggering rate—one breach every six minutes.

Now imagine a different kind of nightmare. You walk into the office on a Monday morning, just one week before a major tax deadline, and find that none of your client files will open. Instead, a message glows on every computer screen, demanding a massive payment in cryptocurrency to get your data back. Your entire firm is frozen.

Client financials, tax software, and every essential record are encrypted and held hostage.

This is a ransomware attack, and for an accounting firm, the timing couldn't be more devastating. Cybercriminals know your calendar and deliberately launch these attacks during your busiest seasons to apply maximum pressure. The choice they give you is brutal: pay the ransom and hope they return your data, or face catastrophic operational failure, client loss, and permanent damage to your reputation. The ransom itself is often secondary to the crippling loss of productivity and client trust.

For a deeper dive, our guide on how to prevent ransomware attacks offers proactive strategies to keep your data safe.

Not all threats come from shadowy hackers halfway across the world. Sometimes, the most damaging breaches start from within—and often, they're completely accidental.

An employee trying to be productive from home might save sensitive client tax returns to a personal, unsecured USB drive and then lose it. Another might fall for a simple phishing email and unknowingly type their login credentials into a fake website, handing an attacker the keys to your entire network.

These insider threats are particularly tricky because they bypass traditional security like firewalls. Whether driven by malicious intent or simple human error, a single mistake can expose your whole client database. This is why ongoing employee training and clear, enforceable security policies are so critical. Every single person on your team has a role to play in protecting the firm's—and its clients'—most sensitive information.

For most accountants, compliance regulations feel like a dense maze of legal jargon. But rules like the FTC Safeguards Rule or GDPR aren't just bureaucratic hurdles—they're the blueprints for protecting the sensitive client data that is the lifeblood of your firm. Getting this right is a non-negotiable part of modern cyber security for accountants.

It helps to think of these regulations less as a list of punishments and more as a structured way to earn and maintain client trust. When you demonstrate strong compliance, you’re sending a clear message: "We are responsible, professional guardians of your most confidential information." This isn't just a cost center; it's a powerful competitive advantage.

In today's world, compliance is the baseline for client trust. It transforms a regulatory requirement into a tangible demonstration of your firm's commitment to security, showing clients their data is as important to you as it is to them.

At their core, most data protection regulations boil down to a handful of key principles. Instead of getting lost in the legal text, you can focus on what these rules actually mean for your day-to-day workflow.

Here are the central pillars you need to build into your practice:

Implementing these measures isn't about overhauling your entire operation overnight. It’s about integrating smart, secure habits into your existing processes, turning a regulatory headache into a mark of true professionalism.

For firms handling significant amounts of client data—especially those using cloud services—proving your security posture becomes even more critical. This is where standards like SOC 2 come into play. A SOC 2 report is essentially an independent audit that verifies a service provider securely manages data to protect the interests and privacy of its clients.

It's definitely worth understanding the framework. To get a better handle on the specific requirements and benefits for your firm, check out this guide on What is SOC 2 compliance. It'll help you evaluate vendors and show your own commitment to high security standards.

Choosing partners who are SOC compliant can dramatically simplify your own regulatory burden. For a deeper look into the specifics, you can learn more about what is SOC compliance and how it validates a vendor's security controls, giving you and your clients serious peace of mind. Ultimately, navigating compliance is all about building a culture of security that clients can see and trust.

Knowing the threats and compliance rules is one thing, but building a real defense takes action. This is where the theory gets put to work. A solid cybersecurity strategy for your accounting firm doesn't have to be a nightmare to implement; it's about layering your defenses across three critical areas: Technology, Policy, and People.

This straightforward action plan is designed for any accounting firm to start using today. By breaking it down into manageable steps, you can make real progress in securing your firm's—and your clients'—most sensitive data. Each step gives you the "why it matters" and a "first action to take" to get you moving.

Your technology is the first line of defense. Think of these tools as the locks, alarms, and vaults for your digital assets. Getting them right makes it much harder for attackers to break in and minimizes the damage if they do.

Implement Multi-Factor Authentication (MFA)

Automate Data Backups

Strong policies turn good intentions into consistent, repeatable actions. They are the official playbook your team follows to keep things secure, especially when things go wrong. A clear policy ensures everyone knows their role and what's expected of them.

A well-defined Incident Response Plan is like a fire drill for a cyberattack. You don't want to be figuring out the escape route when the building is already on fire. Planning ahead ensures a calm, coordinated, and effective response.

Develop an Incident Response Plan (IRP)

Establish Clear Access Controls

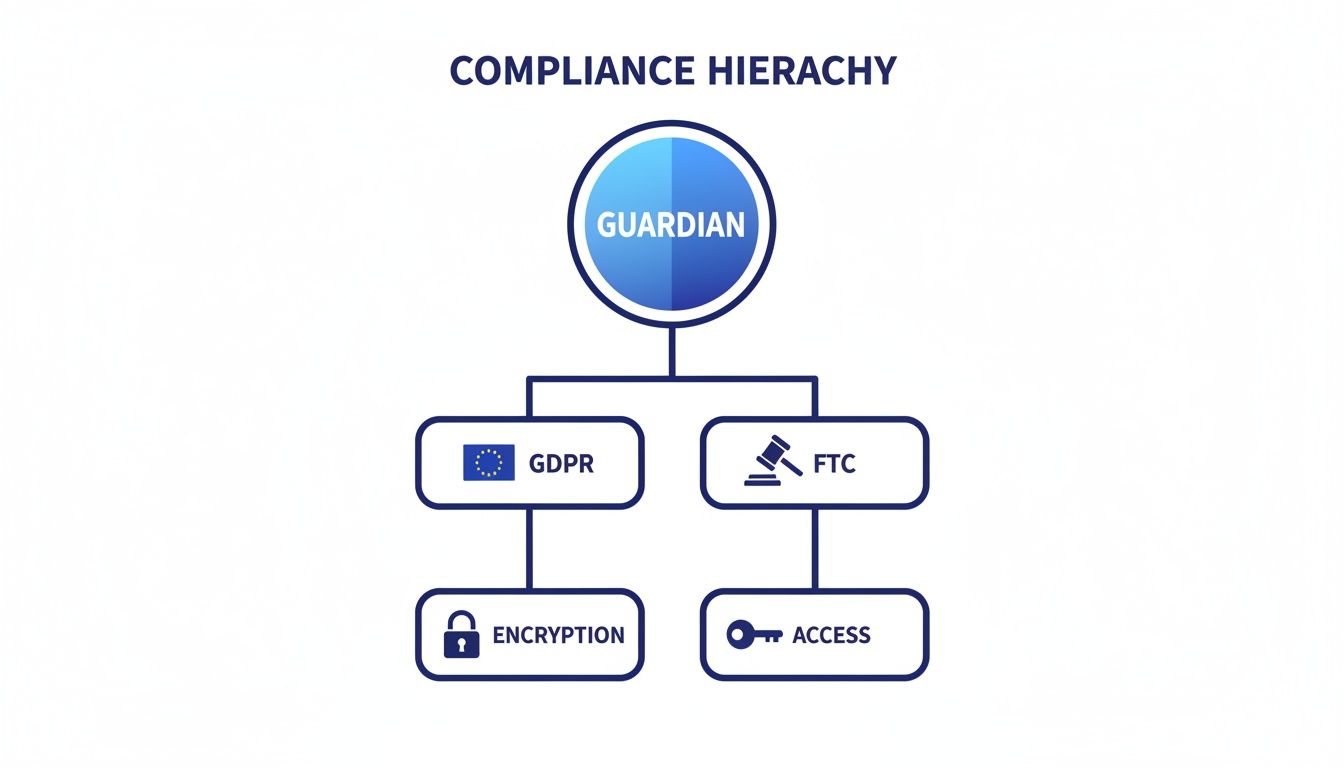

This diagram shows how compliance standards act as a guardian, with frameworks like GDPR and FTC rules guiding foundational security practices like encryption and access control. It illustrates that strong security isn’t just one action but a layered approach where high-level principles are supported by specific, technical controls.

Your employees can be your greatest security asset or your weakest link. The difference comes down to culture and training. A team that understands the threats and knows how to spot them becomes an active part of your defense system.

Conduct Ongoing Security Awareness Training

Run Phishing Simulations

After looking at the threats and the defenses you need, one thing becomes clear: managing cybersecurity in-house is a massive undertaking. The constant cycle of patching, monitoring, and backing up data can easily pull your focus from what you do best—serving your clients.

This is where a strategic shift to a secure cloud hosting environment isn't just an upgrade; it's a game-changer. Imagine offloading the huge burden of physical server security, complex backup schedules, and ensuring 24/7 uptime to a team of specialists. By moving your core applications like QuickBooks, Sage, or your tax software to a secure cloud, you solve multiple security challenges at once.

Running an on-premise server is like being the sole security guard for an entire office building. You’re responsible for the physical locks, the alarm system, the surveillance cameras, and responding to every bump in the night. It's an exhausting, full-time job that demands deep technical expertise most firms just don't have.

A secure cloud hosting provider takes that entire responsibility off your plate. They operate out of enterprise-grade data centers with physical security—like biometric scanners and round-the-clock surveillance—that are miles beyond what a typical accounting firm could afford or implement.

This one move lets you delegate critical security functions, including:

By moving to a dedicated cloud environment, you're not just renting server space; you're adopting an entire security posture that is managed, monitored, and maintained by experts. It’s a fundamental upgrade to your firm's operational resilience.

This shift frees your team to focus on clients, knowing the foundational tech is solid and secure. It’s how you strengthen your firm's cyber security for accountants without having to become IT experts yourselves.

One of the biggest wins with a secure cloud solution is its built-in disaster recovery capability. For firms relying on on-site backups, a ransomware attack or a fire can mean catastrophic data loss. A managed cloud environment completely changes that math.

Reputable providers build automated, daily backups right into their service. These backups are stored securely off-site, creating an “air-gapped” copy of your data that ransomware can't touch even if your local network is compromised. That means you can restore your systems to a clean state with minimal downtime, turning a potential disaster into a manageable hiccup.

Plus, because your applications and data live in the cloud, your firm can keep working from anywhere with an internet connection. If a fire or flood makes your office inaccessible, your team can log in securely from home and keep serving clients without skipping a beat. To see how these systems work, learn more about comprehensive cloud data protection and its role in business continuity.

Flexible work is here to stay, but it brings tough security questions. How do you ensure employees accessing sensitive client files from home are doing it safely? A secure cloud hosting platform creates a centralized, controlled environment for remote access.

Instead of data getting scattered across personal laptops and unsecured home Wi-Fi, everything stays inside the secure cloud. Team members access applications through an encrypted connection, meaning sensitive client information never actually leaves the protected server.

This model makes it much simpler to comply with regulations like the FTC Safeguards Rule, which requires firms to control where and how sensitive data is stored and accessed. By centralizing your data, you create a defensible and auditable security framework that supports modern work styles and your regulatory duties.

We've covered a lot of ground, and the main takeaway is this: cyber threats are a serious reality for accounting firms, but building a secure practice is entirely within your reach. The core message is simple. Proactive cyber security for accountants isn't just an IT task; it's the bedrock of a modern, trustworthy firm. It all comes down to building smart layers of defense across your technology, your policies, and your people.

From the primary attacks targeting your firm to the essential defenses you need to build, it's clear that vigilance is key. It's also clear you don't have to face these complex challenges alone. Empowering your practice means taking a decisive step toward a stronger, more resilient security posture.

A secure, managed cloud environment removes the guesswork from cybersecurity. It provides enterprise-grade protection, allowing you to focus on what you do best—serving your clients with confidence and peace of mind.

This approach simplifies compliance and hardens your defenses all at once.

Building a truly resilient firm is about making strategic decisions that reduce risk and boost operational stability. When you offload the complexities of security management, you gain a significant advantage. Your team can stay productive and secure—whether they're in the office or working remotely—without needing to become cybersecurity experts themselves.

A secure, managed cloud is more than just an IT solution; it's a foundational business strategy. For firms looking to fortify their operations, specialized support is the key to getting it right. Explore how dedicated IT support for accounting firms can provide the expert guidance and infrastructure needed to protect your clients and your reputation. By partnering with specialists, you ensure your firm isn't just surviving but thriving in an increasingly complex digital world.

When it comes to cybersecurity, accountants often have very practical, boots-on-the-ground questions. Here are some of the most common ones we hear, along with straightforward answers.

If you only do one thing, make it Multi-Factor Authentication (MFA). Think of it as a digital deadbolt for your most sensitive accounts. It requires your password plus a second piece of proof, like a code sent to your phone, before granting access.

This one step is astonishingly effective. It shuts down the vast majority of automated attacks that rely on stolen passwords, making it exponentially harder for a criminal to get into your email, client portal, or practice management software. For the impact it has, it’s the cheapest and easiest security measure you can possibly implement.

The FTC Safeguards Rule isn't just a suggestion; it demands a written security plan and the technical safeguards to back it up. This is where a secure cloud hosting provider can lift a huge weight off your shoulders.

A reputable cloud provider builds its entire service around compliance. They have the enterprise-grade firewalls, the data encryption, and the documented disaster recovery plans that the FTC wants to see. This lets you offload a massive technical and administrative burden.

Instead of building it all from scratch, you get to lean on their secure infrastructure. You can then reference their controls directly in your own security plan, which makes demonstrating due diligence much, much simpler.

An annual memo about phishing just doesn’t cut it. To build a team that’s genuinely security-aware, you need training that is consistent, engaging, and feels real.

Here are a few ideas that actually work:

When training is relevant and interactive, you empower your team to become your strongest asset against these kinds of attacks.

At Cloudvara, we provide a secure, managed cloud environment that simplifies compliance and hardens your defenses, allowing you to focus on your clients with confidence. Learn how our tailored solutions can protect your practice. Find out more at https://cloudvara.com.