Starting a CPA firm isn't just about being a great accountant—it's about becoming a business owner. The real key is building a solid foundation from day one, which means choosing the right legal structure, getting essential insurance, and defining a specific client niche you can truly own.

Moving from technical accounting work to firm ownership requires a major mental shift. You're no longer just crunching numbers for others; you're building a valuable asset for yourself. The initial decisions you make about your business plan, legal entity, and financial setup will shape your firm’s path for years to come.

Think of it like laying the groundwork for a skyscraper. A shaky foundation guarantees problems down the road. A solid, well-planned base, on the other hand, is what supports future growth and stability.

A business plan is so much more than a document you show a lender. It's your operational roadmap. It forces you to get crystal clear about who you serve and, just as importantly, how you'll serve them differently. Generic plans almost always fail because they lack focus.

Instead of trying to be the CPA for all "small businesses," you need to narrow your focus. Seriously consider specializing. For example, you could become the go-to expert for:

A tight niche lets you tailor your marketing, streamline your services, and command premium fees for specialized knowledge. As you hammer out these details, it's incredibly helpful to understand your own position in the market. Exploring some SWOT analysis example guides for small businesses can bring a lot of clarity to your strategic planning.

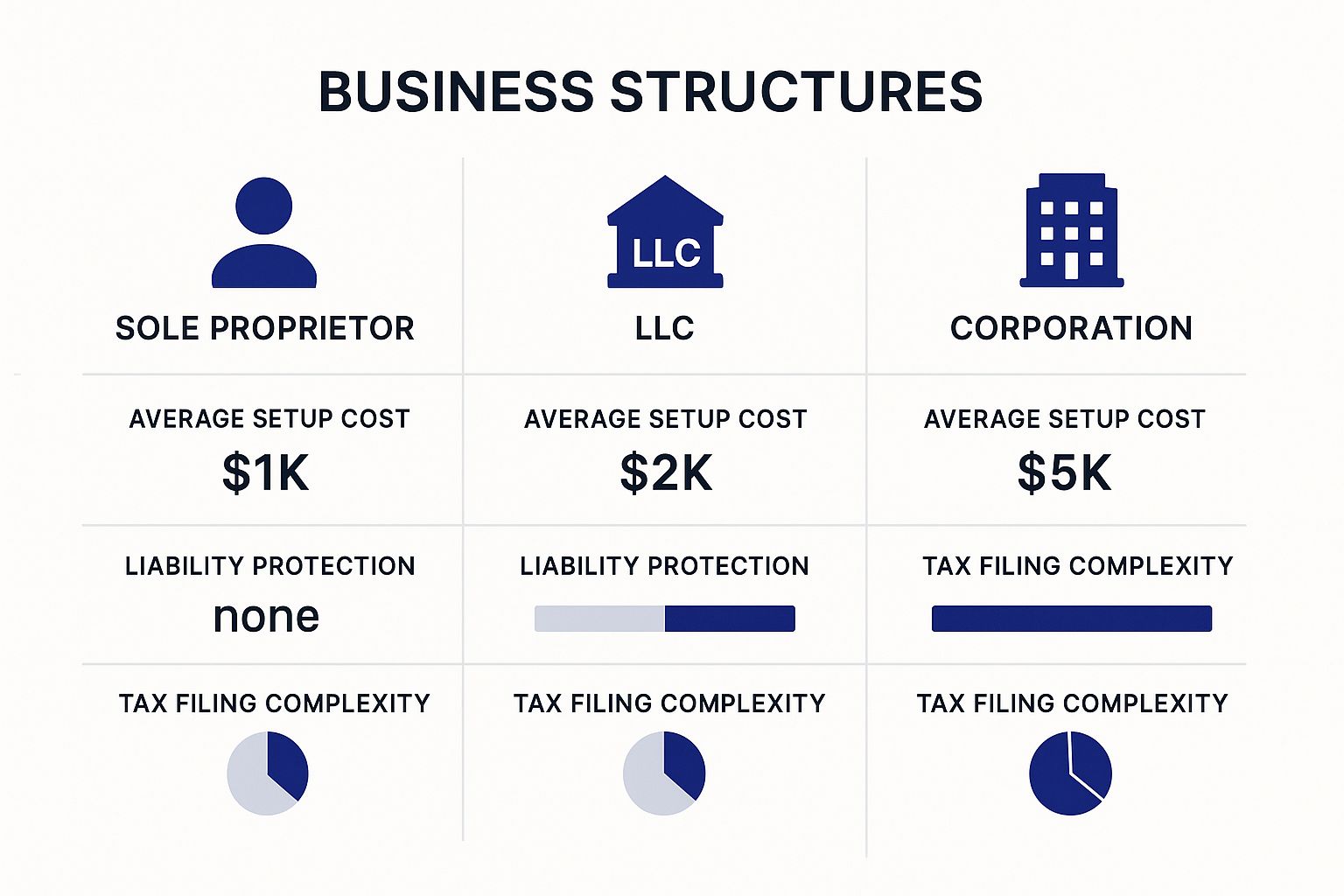

Picking your firm's legal entity is one of the most critical decisions you'll make, affecting everything from personal liability to how much you pay in taxes. Your main options are typically a Sole Proprietorship, an LLC, or an S-Corp.

Key Insight: Most new CPA firm owners gravitate toward an LLC or an S-Corp, and for good reason. These structures provide a crucial liability shield, separating your personal assets from business debts and potential lawsuits—a non-negotiable for any professional services firm.

Making the right choice depends on your goals for liability, taxation, and how much administrative work you're willing to handle. This table breaks down the core differences.

| Structure | Liability Protection | Taxation Method | Best For |

|---|---|---|---|

| Sole Proprietorship | None. Personal and business assets are the same. | Pass-through. Profits/losses reported on personal tax return. | Freelancers or solo practitioners just starting out with very low risk. |

| LLC | Strong. Protects personal assets from business debts. | Flexible. Can be taxed as a sole prop, partnership, or S-Corp. | Most new firms wanting liability protection with less formal requirements. |

| S-Corporation | Strong. Protects personal assets from business debts. | Pass-through with potential for salary/dividend tax savings. | Established firms looking to optimize taxes as profits grow. |

Ultimately, while a sole proprietorship is the simplest to set up, the lack of a liability shield makes it a risky bet for a professional practice. An LLC or S-Corp is almost always the safer, more professional choice.

Once your legal structure is registered, two things are non-negotiable: professional liability insurance and a dedicated business bank account. Get these sorted out immediately.

Errors and Omissions (E&O) insurance is your safety net. It protects your firm if a client claims a mistake on your part caused them financial harm. It isn't just a smart move; many state licensing boards require it.

Opening separate bank and credit card accounts for the firm is just as critical. Mingling personal and business funds is a rookie mistake that can "pierce the corporate veil," destroying the liability protection of your LLC or S-Corp and putting your personal assets on the line. This simple step is vital for clean books and maintaining your legal shield.

When you're launching a new CPA practice, your technology stack isn't just a line item on your budget—it’s the engine that will drive your firm’s efficiency, security, and client experience. Getting this right from day one saves you from the massive headaches of data migrations and clunky workflows down the road. The goal is to build an integrated system that automates the grunt work, freeing you up for high-value client advisory.

Forget the days of needing a dedicated server room with its costly hardware and constant maintenance. For a new firm, cloud-based solutions are the only way to go. They give you secure, flexible access to your firm’s data from anywhere, on any device. That’s not a luxury anymore; it's essential for serving clients and running your business on your own terms.

Your tech stack will be built around a few core software categories. While the specific brands you choose will depend on your budget and niche, their functions are fundamental to running a modern practice.

To get started, here's a look at the essential software categories every modern CPA firm needs, along with some of the most popular options available today.

| Software Category | Key Function | Popular Examples |

|---|---|---|

| Tax Preparation | The heart of your compliance services, handling federal and state forms for individuals and businesses. | Drake Tax, UltraTax CS, Lacerte Tax |

| Accounting | The client-facing software for managing day-to-day bookkeeping and financial reporting. | QuickBooks Online, Xero, Sage |

| Practice Management | Your firm's command center for CRM, project tracking, billing, and workflow automation. | Karbon, Canopy, TaxDome |

| Secure Client Portal | A dedicated, encrypted platform for securely exchanging sensitive financial documents. | ShareFile, SmartVault, Encyro |

Think of these tools as a team. The real magic happens when they work together, eliminating duplicate data entry and streamlining your entire process from engagement to filing.

Key Takeaway: Don't buy software in silos. The best tech stacks are deeply integrated. Your practice management tool should talk to your accounting software, and your client portal should sync seamlessly with your document management system. Integration is what creates a truly smooth workflow.

While many tools are born in the cloud, some of the most powerful desktop applications—like certain versions of QuickBooks—are not. This is where cloud hosting becomes a critical piece of the puzzle. It lets you run traditional desktop software in a secure, accessible cloud environment.

This approach delivers the best of both worlds: you get the robust functionality of desktop applications combined with the remote access and security benefits of the cloud. For instance, using a specialized service for cloud hosting for QuickBooks allows your team and even your clients to access the same company file in real-time without being chained to a specific office computer.

This kind of flexibility is crucial. By 2025, the global accounting services market is projected to hit a staggering $735.94 billion. A major driver of this growth is technology adoption, with 61% of accountants viewing AI as a key opportunity to improve their work, according to recent industry analysis from LinkMyBooks. A cloud-based foundation is what will allow you to capitalize on these shifts.

With so many options out there, choosing the right software can feel overwhelming. My advice? Focus on vendors that specialize in serving accounting professionals. Their features will be tailored to your specific workflows and compliance needs.

Here are a few things I always check before committing to a new tool:

Investing thoughtfully in your technology is an investment in your firm's future. Choose tools that work together to build an efficient, secure, and client-friendly practice from the ground up.

Figuring out what to sell and what to charge is where the rubber meets the road. How you define and price your services will make or break your firm’s profitability and shape the quality of your client relationships. This isn't just about pulling numbers out of thin air; it’s a strategic choice that defines your brand and ensures you’re paid fairly for the value you deliver.

One of the biggest mental hurdles for new firm owners is moving past the billable hour. It’s familiar, sure, but it punishes you for being efficient and creates tension with clients who live in fear of surprise invoices. The best way to build a sustainable practice is with a clear service menu and transparent pricing.

You’ve got three main ways to bill for your work, and honestly, most successful firms mix and match them depending on the project.

Most new CPAs find their footing by starting with fixed-fee pricing. It’s a straightforward transition from hourly and brings immediate clarity to your client proposals.

Expert Insight: Don't get stuck on one model. Start with fixed-fee packages for your compliance services and dip your toes into value-based pricing for high-impact advisory projects. The most important thing is being upfront about how you charge from day one.

Bundling your services into tiered packages is one of the smartest moves you can make. It simplifies the sales pitch for you and makes the buying decision a no-brainer for your clients. Even better, it creates the predictable, recurring revenue that is the lifeblood of any healthy firm.

For a small business client, a tiered structure might look something like this:

This structure lets clients pick the service level that fits their needs and gives you a clear path to grow with them. You’re no longer just the once-a-year tax preparer; you’re their trusted, year-round advisor. To deliver these services well, your tech stack is key. Having solid cloud accounting solutions is non-negotiable for managing client data securely and efficiently across all your packages.

Calculating your rates is a real science. Start by adding up all your annual overhead—your software, insurance, marketing, and any office costs. Then, add your target salary and a healthy profit margin. Aim for at least 20-30% to start. Divide that grand total by your realistic billable hours for the year, and you’ll have a baseline rate to build your fixed-fee packages from.

Once a price is agreed upon, your engagement letter is your new best friend. It’s not a formality; it’s a binding agreement that clearly spells everything out:

A rock-solid engagement letter is your single best defense against "scope creep"—that familiar story where a small project mysteriously balloons into a massive, unpaid time suck. It sets professional boundaries from the very first handshake.

Let's be blunt: an amazing firm with powerful technology and perfect service packages is still just a business plan without clients. Marketing isn't something you bolt on at the end; it’s the engine that turns your expertise into revenue.

The good news? You don't need a massive budget or flashy Super Bowl ads to win those first critical clients. Modern marketing for a professional service firm is about building trust and demonstrating value, not shouting the loudest. It’s a game of targeted outreach and establishing yourself as the go-to authority in your niche. Your goal is to create a steady stream of qualified leads who already see you as the expert they need.

Your website is your digital storefront. It doesn’t need to be a complex, ten-thousand-dollar masterpiece, but it absolutely must be professional, easy to navigate, and crystal clear about who you help and how. Think of it as your 24/7 salesperson.

A simple, effective website needs just a few core pages:

This is your firm's online headquarters. It’s where prospects go to check you out after hearing your name, and it’s where all your other marketing efforts will ultimately lead them.

One of the most powerful ways to attract ideal clients is by answering the specific questions they're already typing into Google. This is the heart of content marketing and search engine optimization (SEO) for accountants. You create genuinely helpful articles that solve precise pain points.

Forget generic posts like "Tax Tips for Small Business." Get specific. Real-world examples might look like:

These kinds of articles attract high-intent searchers who need your exact expertise. As you build your firm's infrastructure, think about how your IT choices can support this. Running your systems on a secure cloud platform ensures your team can collaborate on content and client work from anywhere. It's also smart to understand the transparent cloud hosting pricing so you can budget for it effectively from the start.

Key Insight: You are not just writing a blog; you are building a library of lead-generating assets. Each targeted article acts as a permanent magnet, pulling in your ideal clients around the clock, for years to come.

While digital marketing is essential, don't ever underestimate the power of good old-fashioned networking—just with a modern twist. I can almost guarantee your first few clients will come from your existing network or referrals.

LinkedIn is your primary tool here. Focus on building strategic connections with professionals who serve the same clients but don't compete with you. Think about:

Connect with these folks in your geographic area or niche. And please, don't just send a generic connection request. Personalize it. Mention a shared connection, a piece of content they shared, or a local event. The goal is to build a reciprocal relationship where you become their go-to CPA referral. For a deeper dive, this ultimate B2B lead generation playbook offers some fantastic, actionable insights.

Nothing convinces a hesitant prospect like seeing that other people already trust you. Social proof is the secret sauce that turns a "maybe" into a signed engagement letter. You need to be systematic about collecting it from day one.

Once you’ve successfully wrapped up a project or a tax season for a happy client, make it part of your offboarding process to ask for a review or testimonial. Make it easy for them. Send a direct link to your Google Business Profile or LinkedIn page. Displaying these glowing reviews prominently on your website builds immediate credibility and makes winning that next client so much easier.

Landing your first few clients is a huge win. But the real test isn't getting to five clients—it's building a firm that can gracefully handle fifty without everything catching fire. Scaling a CPA practice is a deliberate act, not an accident. It's about engineering an operational machine that grows revenue without forcing you to work 80-hour weeks.

The shift from being a solo practitioner to a true business owner happens the moment you start working on your business, not just in it. This means stepping back from the daily grind to build the processes and infrastructure that fuel sustainable, profitable growth. It’s about designing a firm that runs smoothly, whether you're at your desk or on vacation.

The secret to delivering consistent, high-quality service as you grow is documentation. What feels like second nature to you is a complete mystery to a new hire or contractor. You have to get your core processes out of your head and onto paper (or, more likely, a digital document).

Start by mapping out your most critical workflows. Think step-by-step:

Documenting these processes creates a playbook for your firm. It ensures every client gets the same stellar experience and makes it infinitely easier to hand off tasks when you bring on help.

As your workload piles up, you'll hit a major crossroads: do you hire your first W-2 employee or bring in a freelance contractor? There’s no single right answer here. The best choice hinges on your firm's immediate needs, cash flow, and long-term vision.

| Factor | Hiring an Employee | Using a Contractor |

|---|---|---|

| Cost | Higher upfront cost (salary, benefits, payroll taxes, workers' comp). | Generally lower cost, paid per project or hour with no overhead. |

| Control & Integration | You have more control over their work, schedule, and training. They become part of your firm's culture. | Less control. They operate as an independent business with their own methods. |

| Flexibility | Less flexible. Hiring and firing are complex legal processes. | Highly flexible. You can scale their hours up or down based on seasonal demand. |

| Work Scope | Can perform a wide range of tasks, including administrative and client-facing duties. | Typically hired for a specific, specialized task like complex tax prep or bookkeeping. |

For most new firms, starting with a contractor is a smart, low-risk move. It lets you get much-needed help without taking on the significant financial and administrative weight of a full-time employee.

Expert Tip: Before you hire anyone, map out the exact tasks you want to delegate. Start by offloading the lower-value, time-consuming work first. This frees you up to focus on high-impact activities like client strategy and business development.

The modern way to scale a CPA firm isn't just about throwing more people at the problem. It’s about using technology to get more done with the team you already have. Growth strategies today are all about pairing an expanding client base with smart tech and automation.

In fact, a 2025 report reveals that nearly 65% of firms plan to grow using this exact combination. Strikingly, only 21% plan to increase headcount, a huge drop from 35% the previous year. This signals a massive shift toward efficiency over just hiring more bodies. You can dig into the details by reading the full report on the 2025 state of tax professionals.

This is where your technology stack truly starts to pay off. Your practice management software can automate task assignments and deadline reminders. Your client portal can automate document requests. These small efficiencies compound over time, allowing you to handle a bigger workload without a proportional jump in manual effort. As your firm grows, it's worth exploring the top benefits of cloud computing for SMEs to see how a flexible infrastructure is built to support this automated approach.

Finally, remember that one of the most powerful—and most overlooked—scaling strategies is to deepen your existing client relationships. It's far easier and more profitable to sell a new service to a happy, current client than it is to chase down a brand new one.

Review your client list regularly. Is there a tax planning client who could benefit from your monthly bookkeeping? Do you have a bookkeeping client who’s ready for higher-level CFO advisory work? Proactively spotting these opportunities opens up new revenue streams and makes you an indispensable partner to your best clients. Better yet, happy clients become your most powerful referral source, creating a virtuous cycle of sustainable growth.

Building a firm from the ground up brings a wave of questions. I’ve been there, and so have countless other CPAs. To help you push forward with confidence and sidestep the common pitfalls, we've pulled together some straight answers based on real-world experience.

Startup costs swing wildly. You could get a lean, home-based practice off the ground for a few thousand dollars. On the other hand, if you’re leasing an office and hiring from day one, you could easily be looking at $25,000 or more. There’s no single magic number.

Regardless of your path, some initial expenses are unavoidable:

The biggest fork in the road is your physical footprint. A remote-first model slashes your startup capital needs, freeing up cash to pour into better technology and marketing. This approach lives or dies by its tech foundation, so understanding what cloud accounting is is the first step to building that remote infrastructure the right way.

It’s so tempting to be a generalist and cast the widest net possible. I get it. But specializing is one of the fastest routes to building authority and, frankly, becoming more profitable. When you focus on a specific niche—say, e-commerce brands, real estate investors, or healthcare practices—you stop being a commodity.

Real-World Impact: A niche focus lets you tailor every piece of marketing to a client’s exact pain points. You become the obvious choice because your website and content speak their language, showing you understand their unique world in a way a generalist never could.

You'll develop deeper expertise, streamline your workflows, and command higher fees. It feels counterintuitive to shrink your potential market, but specialization is the strategy that attracts higher-value clients who are actively looking for a true expert.

Forget about complex marketing funnels for a minute. Your first few clients will almost certainly come from your existing professional network. This is where years of building a good reputation and solid relationships pay off instantly.

Start by having conversations with people who already know, like, and trust you. This means former colleagues, key contacts on LinkedIn, local business owners you know, and professionals in adjacent fields like law or financial planning.

Offer a free initial consultation. Your only goal at this stage is to demonstrate value and build trust. Show them you can solve their problems, and the business will follow.

Absolutely. In fact, this is an incredibly common and practical way to get started. Launching your firm as a side business gives you a financial safety net, allowing you to build a client base and test your business model without the immense pressure of needing immediate revenue to cover your personal bills.

Be warned, though: this path requires exceptional discipline and time management. You have to be ready for long evenings and weekends as you serve your first clients while keeping up performance at your day job. It’s critical to set clear, specific milestones for when you’ll make the leap to working on the firm full-time.

Ready to build your firm on a secure, scalable, and reliable cloud foundation? Cloudvara centralizes all your essential applications—from tax software to QuickBooks—onto a secure platform accessible from anywhere. Reduce IT costs, ensure business continuity, and focus on what you do best. Start your free 15-day trial today and see the difference.